Roth IRA vs Traditional IRA: Which Is Better for Retirement?

Planning for retirement can feel like navigating a maze, especially when trying to decipher the best way to save. The financial world throws around terms like "Roth IRA" and "Traditional IRA" without always explaining what they mean or which one might be right for you. It's easy to feel lost in the jargon, but understanding these retirement savings options is crucial for securing your financial future.

Many people struggle with choosing the right retirement plan. Concerns about taxes, income limits, and future financial stability often lead to confusion and hesitation. Will you pay more in taxes now, or later? What if your income changes? These are valid questions that deserve clear, straightforward answers.

The question of which is better, a Roth IRA or a Traditional IRA, depends entirely on your individual circumstances and financial goals. There's no one-size-fits-all answer. This article aims to demystify these two popular retirement savings vehicles, helping you understand their differences, benefits, and drawbacks so you can make an informed decision that aligns with your unique situation.

In essence, a Roth IRA offers tax-free withdrawals in retirement, while a Traditional IRA provides a tax deduction now but taxes your withdrawals later. Understanding your current and projected income, tax bracket, and risk tolerance are key to determining which IRA is the right fit for you. We'll explore the nuances of each, looking at contribution limits, eligibility requirements, and potential tax implications to empower you to make the best choice for your golden years. It will delve into the advantages of each option, touching upon topics such as contribution limits, eligibility criteria, and the possible tax consequences of making an informed decision regarding retirement savings.

Understanding Your Financial Situation

Choosing between a Roth and Traditional IRA feels like a guessing game if you don't understand your current financial picture. I remember when I first started thinking about retirement, I just picked the one my friend recommended without really considering my own needs. Big mistake! I ended up switching a few years later because it wasn't the best fit for my income situation at the time.

Before diving into the specifics of each IRA, take a moment to assess your current income and expenses. Are you in a low tax bracket now? Do you anticipate your income increasing significantly in the future? If you're in a lower tax bracket now, a Roth IRA might be more advantageous, as you'll pay taxes on your contributions now when your tax rate is lower, and then enjoy tax-free withdrawals in retirement. Conversely, if you expect to be in a lower tax bracket in retirement, a Traditional IRA might be better, as you'll get a tax deduction now and pay taxes on your withdrawals later when your tax rate is lower.

Consider factors like your age, career trajectory, and any major life events on the horizon. Are you planning to start a family, buy a house, or change careers? These events can significantly impact your income and tax bracket, influencing which IRA aligns better with your long-term financial goals. Also, think about your risk tolerance. Both Roth and Traditional IRAs offer a variety of investment options, but understanding your comfort level with risk is essential for building a retirement portfolio that you're comfortable with.

Roth IRA vs. Traditional IRA: The Basics

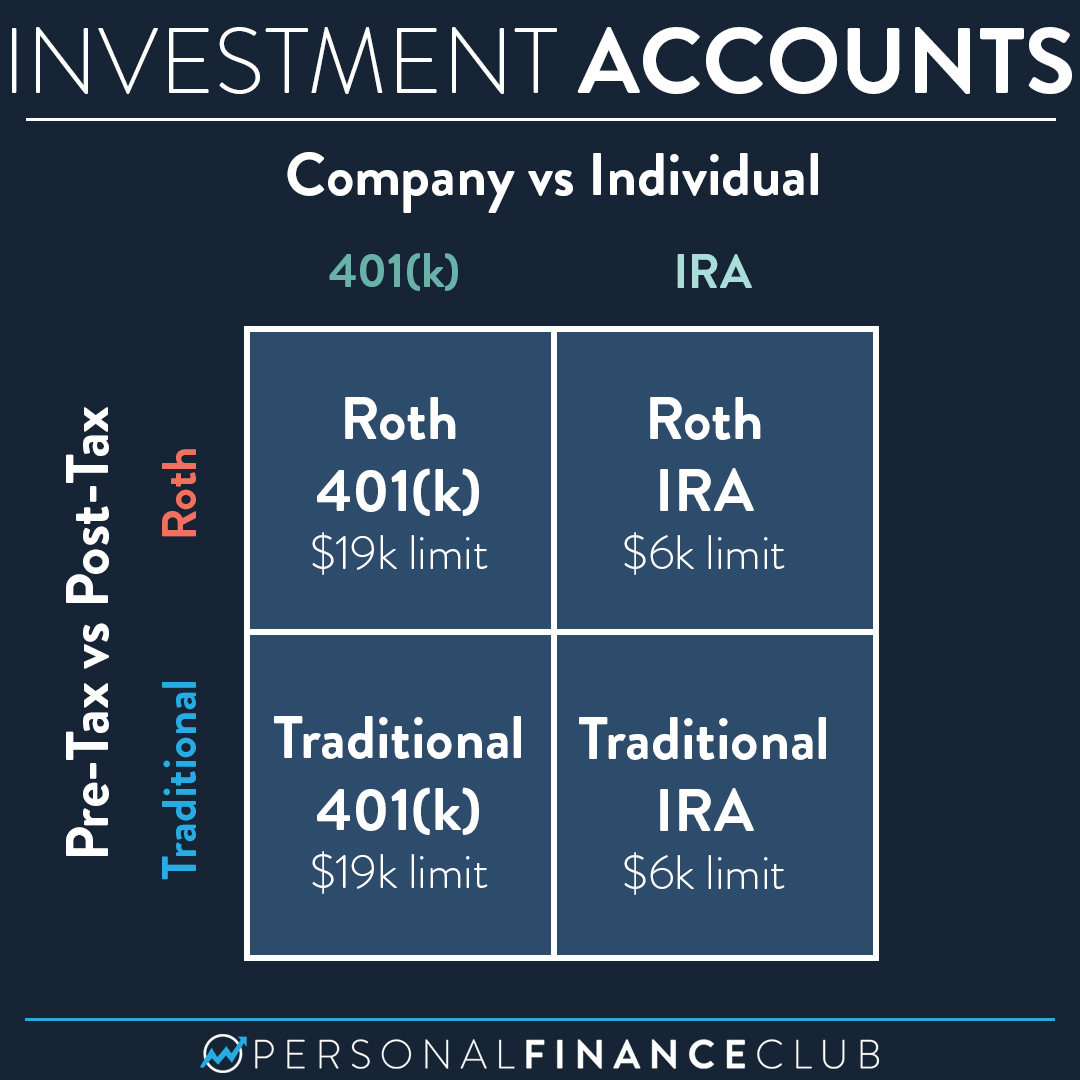

Okay, let's break down the fundamentals. A Traditional IRA is a retirement account that allows you to contribute pre-tax dollars, meaning you can deduct your contributions from your taxable income in the year you make them. This can lower your current tax bill. However, when you withdraw the money in retirement, those withdrawals are taxed as ordinary income. Think of it as postponing your taxes.

A Roth IRA, on the other hand, is funded with after-tax dollars. You don't get a tax deduction for your contributions, but the beauty of a Roth IRA is that your investments grow tax-free, and withdrawals in retirement are also tax-free. This can be a huge advantage if you anticipate being in a higher tax bracket in retirement.

Think about it like this: with a Traditional IRA, you get a tax break now, but pay taxes later. With a Roth IRA, you pay taxes now, but get tax-free income later. Both options have contribution limits, which are subject to change each year. Also, it is important to remember that each has eligibility requirements. High-income earners may not be eligible to contribute to a Roth IRA directly, but there are ways around this, such as the backdoor Roth IRA strategy, which we will discuss later. Furthermore, the traditional IRA does not allow Roth IRA contributions, and vice versa.

The History and Myths of IRAs

The history of IRAs is quite interesting. They were first introduced in 1974 as part of the Employee Retirement Income Security Act (ERISA) to encourage individuals to save for retirement. The Roth IRA came along much later, in 1997, offering a new tax-advantaged way to save.

One common myth is that you can only have one type of IRA. That's not true! You can have both a Roth and a Traditional IRA, as long as you meet the eligibility requirements and don't exceed the annual contribution limits across all your IRA accounts. Another myth is that IRAs are only for employees. Self-employed individuals can also contribute to IRAs, and there are even SEP IRAs and SIMPLE IRAs specifically designed for small business owners and the self-employed.

Some people believe that IRAs are too complicated to understand, which prevents them from getting started. While the rules and regulations can seem daunting, the basic concept is simple: save money now for retirement and enjoy tax advantages. There are plenty of resources available to help you learn more, including financial advisors, online articles, and educational workshops. So, don't let the perceived complexity scare you away from taking control of your retirement savings. Seek advice from financial advisors.

Unveiling the Hidden Secrets of IRAs

One of the best-kept secrets about IRAs is the power of compounding. When your investments grow tax-deferred (Traditional IRA) or tax-free (Roth IRA), the earnings generate even more earnings over time. This compounding effect can significantly boost your retirement savings, especially if you start early.

Another secret is the backdoor Roth IRA strategy. As mentioned earlier, high-income earners may not be eligible to contribute to a Roth IRA directly. However, they can contribute to a non-deductible Traditional IRA and then convert it to a Roth IRA. This allows them to take advantage of the tax-free growth and withdrawals of a Roth IRA, even if their income exceeds the eligibility limits. It's a bit of a loophole, but it's perfectly legal and can be a valuable tool for high-income savers.

Also, remember that IRAs offer creditor protection in many states. This means that your IRA assets are generally protected from lawsuits and creditors. This can provide peace of mind knowing that your retirement savings are safe, even if you face financial challenges in the future. Consult with a qualified legal professional to understand the specific creditor protection laws in your state. A Roth IRA conversion is not for everyone, be sure to seek professional advice.

Recommendations for Choosing the Right IRA

Okay, so how do you actually decide which IRA is right for you? First, consider your current and projected income. If you expect to be in a higher tax bracket in retirement, a Roth IRA is likely the better choice. If you expect to be in a lower tax bracket, a Traditional IRA might be more advantageous. However, predicting the future is never easy, so it's important to consider other factors as well.

Think about your risk tolerance and investment goals. Both Roth and Traditional IRAs offer a variety of investment options, from stocks and bonds to mutual funds and ETFs. Choose investments that align with your risk tolerance and time horizon. If you're young and have a long time until retirement, you can afford to take on more risk. If you're closer to retirement, you might want to consider a more conservative approach. The key is diversification, which involves spreading your investments across different asset classes to reduce risk.

Don't be afraid to seek professional advice from a financial advisor. A qualified advisor can help you assess your financial situation, understand your options, and develop a retirement savings plan that meets your individual needs and goals. They can also provide guidance on investment selection and tax planning. Roth IRA withdrawals are tax-free.

Contribution Limits and Deadlines

Understanding the contribution limits and deadlines for both Roth and Traditional IRAs is crucial. The IRS sets annual contribution limits, which can change from year to year. Be sure to check the current limits before making your contributions. For 2023, the contribution limit for both Roth and Traditional IRAs is $6,500, with an additional $1,000 catch-up contribution for those age 50 and older.

The deadline for contributing to an IRA for a particular tax year is typically April 15th of the following year. This means you have until tax day to make contributions that count towards the previous year's limit. Don't wait until the last minute, though. It's always a good idea to contribute early and often to take full advantage of the tax benefits and the power of compounding.

Also, be aware of the income limits for contributing to a Roth IRA. If your income exceeds a certain threshold, you may not be eligible to contribute directly to a Roth IRA. As mentioned earlier, the backdoor Roth IRA strategy can be a workaround for high-income earners, but it's important to understand the rules and regulations before attempting this strategy. Seek advice from financial advisors on Roth IRA early withdrawals.

Tax Implications and Considerations

The tax implications of Roth and Traditional IRAs are the primary difference between the two. With a Traditional IRA, you get a tax deduction for your contributions, which can lower your current tax bill. However, your withdrawals in retirement are taxed as ordinary income.

With a Roth IRA, you don't get a tax deduction for your contributions, but your withdrawals in retirement are tax-free. This can be a significant advantage if you anticipate being in a higher tax bracket in retirement. Think about your future tax rate.

It's also important to consider the tax implications of converting a Traditional IRA to a Roth IRA. When you convert, you'll have to pay income taxes on the amount you convert. This can be a significant tax burden, so it's important to carefully consider whether a Roth conversion is right for you. Consult with a tax advisor to understand the tax implications of your specific situation. Remember, the primary consideration is the tax advantage of each option.

Early Withdrawal Penalties and Exceptions

Both Roth and Traditional IRAs have penalties for early withdrawals, meaning withdrawals taken before age 59 1/2. Generally, the penalty is 10% of the amount withdrawn, plus you'll have to pay income taxes on the withdrawal from a Traditional IRA.

However, there are some exceptions to the early withdrawal penalty. For example, you can withdraw contributions (but not earnings) from a Roth IRA at any time without penalty or taxes. There are also exceptions for certain qualified expenses, such as medical expenses, education expenses, and first-time home purchases.

It's important to understand these exceptions before making any early withdrawals from your IRA. While it might be tempting to tap into your retirement savings to cover unexpected expenses, it's generally best to avoid early withdrawals if possible to avoid penalties and taxes and to allow your investments to continue growing. Seek advice from financial advisors.

Fun Facts About IRAs

Did you know that the first IRA was created by the Employee Retirement Income Security Act of 1974? It was designed to provide a tax-advantaged way for individuals who weren't covered by employer-sponsored retirement plans to save for retirement.

Another fun fact is that the Roth IRA is named after Senator William Roth of Delaware, who championed the legislation that created it. He believed that it was important to give Americans a tax-free way to save for retirement. Also, remember that Roth IRA is tax-free when you follow regulations.

Finally, did you know that the average IRA balance is significantly lower than the average 401(k) balance? This is likely due to the fact that 401(k)s often have employer matching contributions, which can significantly boost savings. However, IRAs still play a crucial role in retirement planning, especially for those who don't have access to a 401(k) or want to supplement their employer-sponsored plan. Consider both options to maximize your retirement savings.

How to Open and Fund an IRA

Opening and funding an IRA is a relatively simple process. First, you'll need to choose a financial institution, such as a bank, brokerage firm, or credit union. Many institutions offer both Roth and Traditional IRAs. Next, you'll need to complete an application and provide some basic information, such as your name, address, Social Security number, and beneficiary information.

Once your account is opened, you can fund it by making contributions. You can contribute directly from your bank account, or you can transfer funds from another retirement account, such as a 401(k) or another IRA. Be sure to understand the rules and regulations for rollovers and transfers to avoid any tax penalties.

Finally, you'll need to choose your investments. Most financial institutions offer a variety of investment options, such as stocks, bonds, mutual funds, and ETFs. Choose investments that align with your risk tolerance and investment goals. Consider seeking advice from a financial advisor to help you select the right investments for your IRA. Consider the rules and regulations for rollovers.

What If You Contribute Too Much to an IRA?

Contributing too much to an IRA can trigger tax penalties. If you contribute more than the annual contribution limit, the excess contribution is subject to a 6% excise tax each year until you correct the error. It's important to keep track of your contributions and ensure that you don't exceed the limit.

If you accidentally contribute too much, you can correct the error by withdrawing the excess contribution and any earnings attributable to it before the tax filing deadline, including extensions. This will prevent you from having to pay the excise tax. You'll still have to pay income taxes on any earnings you withdraw, but you won't be penalized for the excess contribution. There are many tax professionals who can help you figure out what the tax liability might be.

If you don't correct the error by the tax filing deadline, you'll have to pay the 6% excise tax each year until you withdraw the excess contribution. This can be a costly mistake, so it's important to take steps to prevent it. The IRS provides resources to help you understand the rules and regulations for IRA contributions. Consider this carefully.

Listicle: 5 Key Differences Between Roth and Traditional IRAs

1.Tax Deduction: Traditional IRA contributions may be tax-deductible, while Roth IRA contributions are not.

2.Taxation of Withdrawals: Traditional IRA withdrawals are taxed as ordinary income in retirement, while Roth IRA withdrawals are generally tax-free.

3.Income Limits: Roth IRAs have income limits for contributions, while Traditional IRAs do not (although deductibility may be limited at higher income levels if you're covered by a retirement plan at work).

4.Early Withdrawal Penalties: Both Roth and Traditional IRAs have penalties for early withdrawals, but there are some exceptions for Roth IRAs.

5.Required Minimum Distributions (RMDs): Traditional IRAs require you to start taking RMDs at age 73 (or 75, depending on your birth year), while Roth IRAs do not require RMDs during your lifetime.

Question and Answer

Q: Which IRA is better if I expect my income to increase significantly in the future?

A: A Roth IRA might be more advantageous, as you'll pay taxes on your contributions now when your tax rate is lower, and then enjoy tax-free withdrawals in retirement when your tax rate is potentially higher.

Q: Can I contribute to both a Roth IRA and a Traditional IRA in the same year?

A: Yes, you can contribute to both, but your total contributions across both accounts cannot exceed the annual contribution limit.

Q: What is a "backdoor Roth IRA"?

A: A backdoor Roth IRA is a strategy used by high-income earners who are not eligible to contribute directly to a Roth IRA. They contribute to a non-deductible Traditional IRA and then convert it to a Roth IRA.

Q: Are my IRA assets protected from creditors?

A: In many states, IRA assets are protected from lawsuits and creditors, but the specific laws vary by state. Consult with a qualified legal professional to understand the creditor protection laws in your state.

Conclusion of Roth IRA vs Traditional IRA: Which Is Better for Retirement?

Ultimately, the choice between a Roth IRA and a Traditional IRA depends on your individual circumstances and financial goals. By understanding the differences, benefits, and drawbacks of each option, you can make an informed decision that aligns with your unique situation and helps you secure a comfortable retirement. Whether you prioritize tax deductions now or tax-free withdrawals later, both Roth and Traditional IRAs are valuable tools for building a secure financial future. Remember, the best time to start saving for retirement is now, so take action today to take control of your financial future.

Post a Comment